Fixed vs. Variable Rate Mortgage: Which Is Better for Vancouver Homebuyers Right Now?

If you are looking to buy a home in Vancouver or the Lower Mainland, you have likely found yourself staring at the ceiling at 2:00 AM asking the million-dollar question: Should I choose a fixed or variable rate mortgage?

It is one of the most significant financial decisions you will make during the home-buying process. In a market like Vancouver, where property values are high and mortgages are substantial, the difference between these two options can amount to thousands of dollars in interest savings—or costs—over the life of your loan.

As a native Vancouverite and a mortgage broker with over 15 years of experience, I have seen the market go through every possible cycle. I have helped clients navigate record-low rates, sudden spikes, and everything in between. At Watts Mortgages, my goal isn't just to get you a loan; it's to help you understand how that loan fits into your broader financial picture so you can keep more of your hard-earned money.

In this guide, we will break down the differences between fixed and variable rates, analyze the current landscape in British Columbia, and help you determine which strategy aligns best with your financial goals.

The Great Debate: Stability vs. Potential Savings

Before we dive into the specific strategies for the current Vancouver market, it is crucial to understand the fundamental mechanics of these two mortgage types. They function differently, and they appeal to different types of borrowers.

1. The Fixed Rate Mortgage: The "Sleep Well at Night" Option

A fixed-rate mortgage is exactly what it sounds like. You lock in an interest rate for a specific term (typically 1 to 5 years). During this time, your interest rate and your monthly principal and interest payments remain exactly the same, regardless of what happens to the economy or the Bank of Canada’s benchmark rate.

The Pros:

Budgeting Certainty: You know exactly how much will come out of your bank account every month. This is ideal for first-time homebuyers in Vancouver who are adjusting to the costs of homeownership (strata fees, property taxes, etc.).

Protection from Rate Hikes: If interest rates skyrocket during your term, you are protected. You continue paying your lower, locked-in rate.

Simplicity: It is a "set it and forget it" product.

The Cons:

Higher Initial Rate (Historically): You often pay a "premium" for stability. Lenders price fixed rates based on the bond market and anticipated future risks.

The Penalty Trap: This is the biggest hidden danger. If you need to break a fixed-rate mortgage early (e.g., you sell your home, separate from a partner, or want to refinance), the penalty is calculated using the Interest Rate Differential (IRD). In a falling rate environment, this penalty can be astronomical—sometimes tens of thousands of dollars.

No Benefit from Rate Drops: If rates fall significantly, you are stuck paying the higher rate until your term renews.

2. The Variable Rate Mortgage: The "Ride the Market" Option

A variable-rate mortgage fluctuates with the lender’s Prime Rate, which is directly influenced by the Bank of Canada. While your interest rate can change, your relationship with the payment depends on the specific product (Adjustable vs. Variable).

The Pros:

Historically Lower Costs: Over the last 20+ years, studies have shown that variable-rate holders often save money compared to fixed-rate holders, although past performance does not guarantee future results.

Lower Penalties: Breaking a variable mortgage is usually much cheaper and more predictable. The penalty is typically just three months' interest. This offers incredible flexibility if you plan to move or refinance sooner than expected.

Benefit from Rate Cuts: If the Bank of Canada cuts rates to stimulate the economy, your interest costs go down immediately.

The Cons:

Uncertainty: Your rate can rise. If inflation spikes and the central bank raises rates, your interest costs increase.

Payment Fluctuation (Adjustable Rate Mortgages): With some lenders, if the rate goes up, your monthly payment goes up immediately to cover the extra interest.

Trigger Rates (Static Payment Variable Mortgages): With other lenders, your payment stays the same, but the portion going toward interest increases while the principal pay-down decreases. If rates rise high enough, you may hit a "trigger rate" where your payment no longer covers the interest, forcing a payment increase or lump sum payment.

Current Market Context: Buying in Vancouver

Why does this choice matter so much right now for Vancouverites? Because our mortgages are larger than the national average.

When you have a $800,000 or $1,000,000 mortgage—common for detached homes in North Vancouver or condos downtown—a 0.50% difference in interest rate translates to significant monthly cash flow. Furthermore, the Vancouver market moves fast. You need a mortgage that allows you to pivot if your life circumstances change.

The "Spread" Matters:

When comparing fixed vs. variable, we look at the "spread"—the difference between the offered fixed rate and the offered variable rate. If the variable rate is significantly lower than the fixed rate, it provides a buffer against potential rate hikes. If the variable rate is very close to (or higher than) the fixed rate, the incentive to take on the risk diminishes unless you value the flexibility of the lower break penalty.

Comparison: Fixed vs. Variable at a Glance

To help you visualize the differences, here is a comparison based on typical loan features.

| Feature | Fixed Rate Mortgage | Variable Rate Mortgage |

| Interest Rate | Stays the same for the entire term. | Fluctuates with the Prime Rate. |

| Monthly Payments | Predictable and unchanging. | May fluctuate or change in principal/interest composition. |

| Penalty to Break | High Risk: Interest Rate Differential (IRD) or 3 months' interest (whichever is higher). | Low Risk: Typically just 3 months' interest. |

| Best For | Risk-averse buyers, tight budgets, and those planning to stay put for 5 years. | Borrowers with flexible budgets, potential to move/refinance, or high risk tolerance. |

| Convertibility | Usually cannot convert to variable without breaking the term. | Can often be converted to a fixed rate at any time without penalty. |

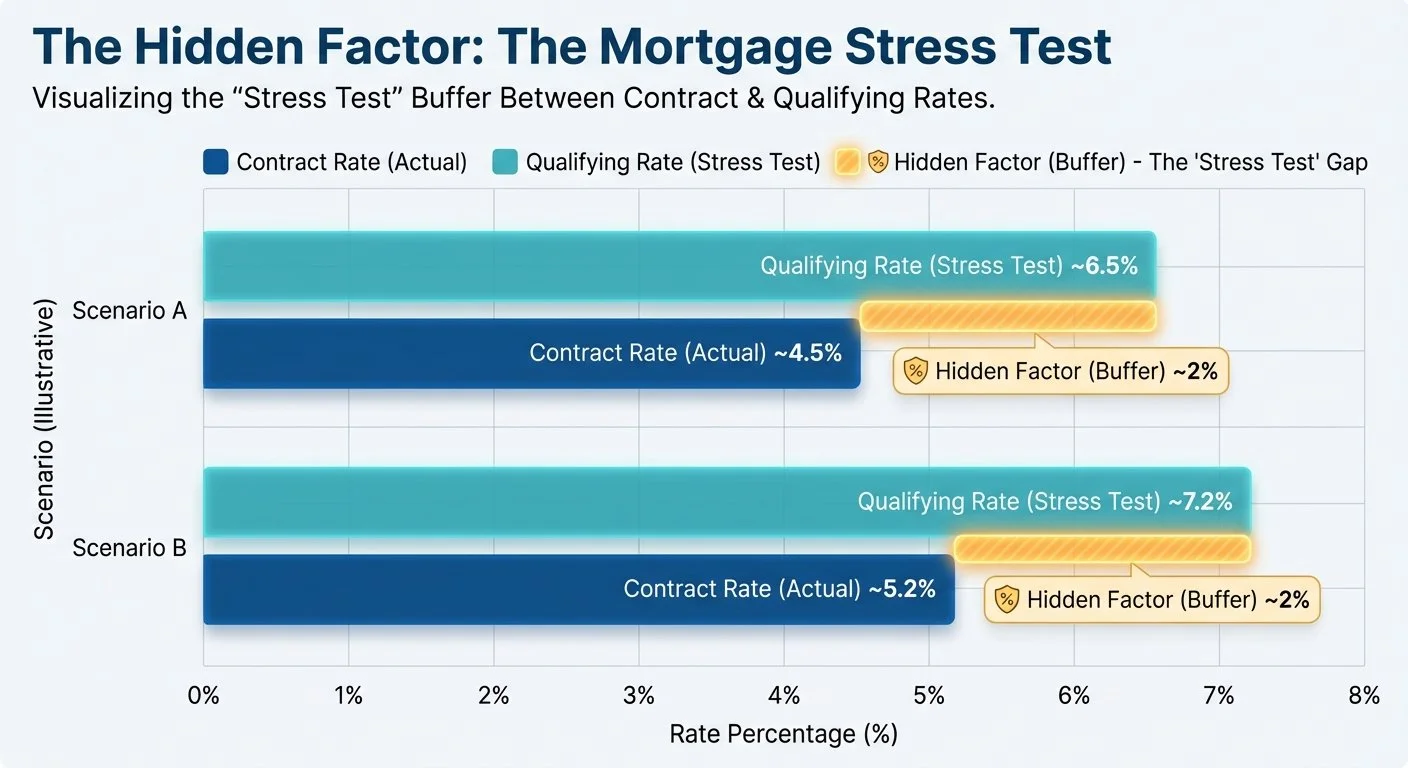

The Hidden Factor: The Mortgage Stress Test

However, your choice of rate does impact your actual monthly cash flow. As a broker with access to over 50 lenders, including those who specialize in private lending or alternative solutions for self-employed individuals, I can help you find lenders with more favorable qualifying criteria if you are pushing the upper limits of your affordability.

Strategic Options: It’s Not Just "5-Year Fixed" vs. "5-Year Variable"

Many homebuyers assume the standard 5-year fixed is the only safe bet. That is simply not true. In a volatile market, we often explore middle-ground strategies.

The Short-Term Fixed Strategy (1-3 Years)

The "Hybrid" Approach

Some lenders allow you to split your mortgage. You could put 50% of your loan on a fixed rate and 50% on a variable rate. This hedges your bet: you get partial protection if rates rise, but you also participate in the savings if rates fall.

Why Working with a Vancouver Mortgage Broker is Crucial

Here is why choosing Chad Watts makes a difference:

Unbiased Advice: I work for you, not the bank. My goal is to find the best solution for your unique needs.

Volume Discounts: Because I deal with millions of dollars in mortgages, I access rates that aren't advertised to the general public.

No Cost to You: For standard residential mortgages, the lender pays my fee. You get expert advice and rate negotiation for free.

Local Expertise: From navigating home-rental purchases to understanding strata properties in Vancouver, I know the local landscape inside and out.

5 Frequently Asked Questions (FAQs)

1. Can I switch from a variable rate to a fixed rate later?

Yes! Most variable-rate mortgages come with a "convertibility feature." This allows you to lock into a fixed rate for the remainder of your term without paying a penalty. This is a great safety net if you choose variable now but lose sleep if rates start to rise.

2. What happens to my variable rate mortgage if the Prime Rate goes down?

If you have an adjustable-rate mortgage (ARM), your monthly payment will decrease immediately. If you have a variable-rate mortgage with static payments (VRM), your monthly payment amount stays the same, but more of that money goes toward paying down your principal, helping you pay off your mortgage faster.

3. Is a fixed rate always safer?

Not necessarily. While it offers payment safety, it carries "penalty risk." If you need to sell your home 3 years into a 5-year fixed term, the Interest Rate Differential (IRD) penalty can be shocking. If you anticipate any life changes (job transfer, growing family, upsizing), a variable rate or a shorter-term fixed rate is often "safer" regarding exit costs.

4. How do I know if I have a "bonafide sales clause" in my low-rate mortgage?

Some "discount" mortgages come with restrictive clauses that prevent you from breaking the mortgage unless you sell the property to an arm's length purchaser. This can trap you. I review all the fine print to ensure you aren't signing a contract that limits your freedom.

5. Should I wait for rates to drop before buying?

Trying to time the market is difficult. While waiting for a lower rate might save you on interest, home prices in Vancouver could rise in the meantime, negating those savings. It is often better to buy when you are financially ready and use a smart mortgage strategy (like a shorter term or variable rate) to take advantage of future rate drops. You can use my Mortgage Calculator to run different scenarios.

Final Thoughts: Which One Is Right for You?

There is no single "best" mortgage for everyone. The right choice depends on your risk tolerance, your budget flexibility, and your future plans.

Choose Fixed if: You lose sleep worrying about the economy, your budget is tight, and you plan to stay in the home for the full term.

Choose Variable if: You can handle some payment fluctuation, you want the flexibility to break the mortgage cheaply, and you believe rates are more likely to trend downward or stay flat.

You don't have to make this decision alone. Navigating the Vancouver housing market is complex, but securing your financing shouldn't be.

Ready to Explore Your Mortgage Options?

Whether you are a first-time buyer, looking to renew, or interested in refinancing to access equity, I am here to help you crunch the numbers.

Let's find the mortgage that fits your life, not just your bank's bottom line.

Call or Text Chad Watts: 778-773-6631

Email: chad@wattsmortgages.ca

Click Here to Schedule Your Free Consultation Today

Disclaimer: The information provided in this blog post is for educational purposes only and does not constitute financial or legal advice. Interest rates and market conditions are subject to change without notice. Please consult with a professional mortgage broker to discuss your specific financial situation.

Chad Watts - Mortgage Broker at TMG The Mortgage Group | Serving Vancouver, North Vancouver, and the Lower Mainland.