First-Time Homebuyer Programs in Vancouver, BC

Entering the Vancouver real estate market for the first time is an exciting milestone, but it can also feel incredibly overwhelming. With shifting interest rates, strict qualification rules, and the competitive nature of the British Columbia housing market, securing your first home requires more than just a down payment—it requires a strategic financing partner. Mortgages have changed, and to succeed, you need the latest solutions tailored to your unique financial situation.

My name is Chad Watts, and as a native Vancouverite and experienced mortgage broker with over 15 years in the industry, I have helped countless clients realize their dream of homeownership. Whether you are looking to buy a condo in downtown Vancouver, a townhome in North Vancouver, or your first family home in the Lower Mainland, there are numerous federal and provincial First-Time Homebuyer Programs designed to help you get into the market faster and more affordably.

On this page, we will explore the top first-time buyer incentives available in BC, how to qualify for them, and how my personalized approach can help you secure the best mortgage terms from my network of over 50 banks and lenders.

Top First-Time Homebuyer Programs in Canada and BC

The Canadian government and the Province of British Columbia offer several powerful programs, tax credits, and incentives to ease the financial burden of buying your first home. Understanding how to leverage these programs together can save you tens of thousands of dollars in taxes and help you maximize your down payment.

1. First Home Savings Account (FHSA)

The First Home Savings Account (FHSA) is one of the most powerful tools introduced for Canadian first-time homebuyers. It combines the best features of a Registered Retirement Savings Plan (RRSP) and a Tax-Free Savings Account (TFSA).

Tax-Deductible Contributions: Like an RRSP, the money you contribute to your FHSA reduces your taxable income for the year, potentially resulting in a significant tax refund.

Tax-Free Withdrawals: Like a TFSA, when you withdraw the funds (including any investment gains) to purchase your first qualifying home, you do not pay any tax on that money.

Contribution Limits: You can contribute up to $8,000 per year, with a lifetime maximum contribution limit of $40,000.

For Vancouver buyers, maximizing the FHSA is a highly effective way to accelerate your down payment savings while reducing your annual tax burden.

2. The Home Buyers' Plan (HBP)

The Home Buyers' Plan allows first-time buyers to withdraw funds from their Registered Retirement Savings Plan (RRSP) to buy or build a qualifying home for themselves or a related person with a disability.

Withdrawal Limit: The federal government recently increased the withdrawal limit to $60,000 per person (up from $35,000). For a couple buying together, this means you can access up to $120,000 tax-free from your RRSPs for your down payment.

Repayment Terms: The funds must be repaid into your RRSP over a 15-year period. However, recent updates have extended the grace period, allowing you to wait up to 5 years before you must begin making repayments.

Combining Programs: You can use the Home Buyers' Plan in conjunction with the FHSA to maximize your available down payment funds.

3. BC First-Time Home Buyers' Program (Property Transfer Tax Exemption)

In British Columbia, purchasers must pay a Property Transfer Tax (PTT) when buying real estate. The PTT is calculated as 1% on the first $200,000, 2% on the portion up to $2,000,000, and 3% on the portion above that. For first-time buyers, the BC government offers an exemption to help offset this significant closing cost.

Full Exemption: Available for purchasing a first home valued up to $500,000.

Partial Exemption: Available for homes valued between $500,000 and $525,000.

Newly Built Home Exemption: Because home prices in Vancouver frequently exceed the $500,000 threshold, many first-time buyers take advantage of the Newly Built Home Exemption. This provides a full PTT exemption on newly constructed homes valued up to $1,100,000, and a partial exemption up to $1,150,000 (limits recently updated by the BC government).

4. First-Time Home Buyers' Tax Credit (HBTC)

Also known as the Home Buyers' Amount, this federal non-refundable tax credit helps first-time buyers recover some of the costs associated with purchasing a home, such as legal fees, home inspections, and land transfer taxes.

Credit Amount: You can claim $10,000 on your personal tax return in the year you purchase your home.

Tax Savings: This translates to a direct tax rebate of $1,500, putting money back in your pocket right when you need it most.

5. GST/HST New Housing Rebate

If your first home is a newly constructed property or a substantially renovated home, you may be subject to paying Goods and Services Tax (GST). The GST/HST New Housing Rebate allows you to recover a portion of the GST paid on the purchase price of the home, provided it is your primary residence and meets specific fair market value thresholds.

Comparing Down Payment Savings Tools

To help you understand the differences between the top savings vehicles, here is a quick comparison table of the FHSA, RRSP (HBP), and TFSA:

Why You Need a Vancouver Mortgage Broker for Your First Home

Many first-time buyers make the mistake of walking directly into their primary bank branch to ask for a mortgage. While your bank may offer you a product, they are limited to selling only their specific mortgage rates and policies. Furthermore, a single bank will not tell you if a competing institution has a better deal.

As an independent mortgage broker in Vancouver and North Vancouver, BC, my priority is you, not the lender. Here is why working with me gives you a distinct advantage:

Access to 50+ Banks and Lenders: I partner with major banks, credit unions, monoline lenders, and private lending options to ensure we find the exact mortgage product that fits your needs.

Unbiased Expert Advice: I evaluate all available options and present you with a variety of mortgage packages. I break down the fine print, including prepayment privileges and penalty calculations, so there are no surprises down the road.

Local Market Expertise: Being a native Vancouverite with 15 years of real estate experience, I understand the nuances of the local market. Whether you're looking at a strata property in Yaletown or a detached home in the suburbs, I know what lenders require for different property types.

Free Service for Borrowers: In the vast majority of traditional residential mortgages, my services are completely free to you. I am compensated directly by the lender who wins your business.

The Mortgage Process for First-Time Buyers: Getting Started is Simple

Step 1: Get to Know You & Comprehensive Consultation

I begin with a comprehensive, no-obligation consultation to understand your financial goals, income, credit history, and long-term plans. We will discuss your ideal monthly budget, explore how much you have saved for a down payment, and review which First-Time Homebuyer Programs you qualify for. This step ensures I tailor my services specifically to your situation.

Step 2: Target a Lender & Secure a Pre-Approval

Step 3: Secure Your Funds & Finalize the Purchase

Once you have an accepted offer on a property, I assist you through the finalization process. I handle the heavy lifting, negotiating with the lender, ensuring all paperwork is completed accurately, and coordinating with your real estate lawyer or notary. With my expert guidance, you’ll secure your mortgage funds quickly and with ease.

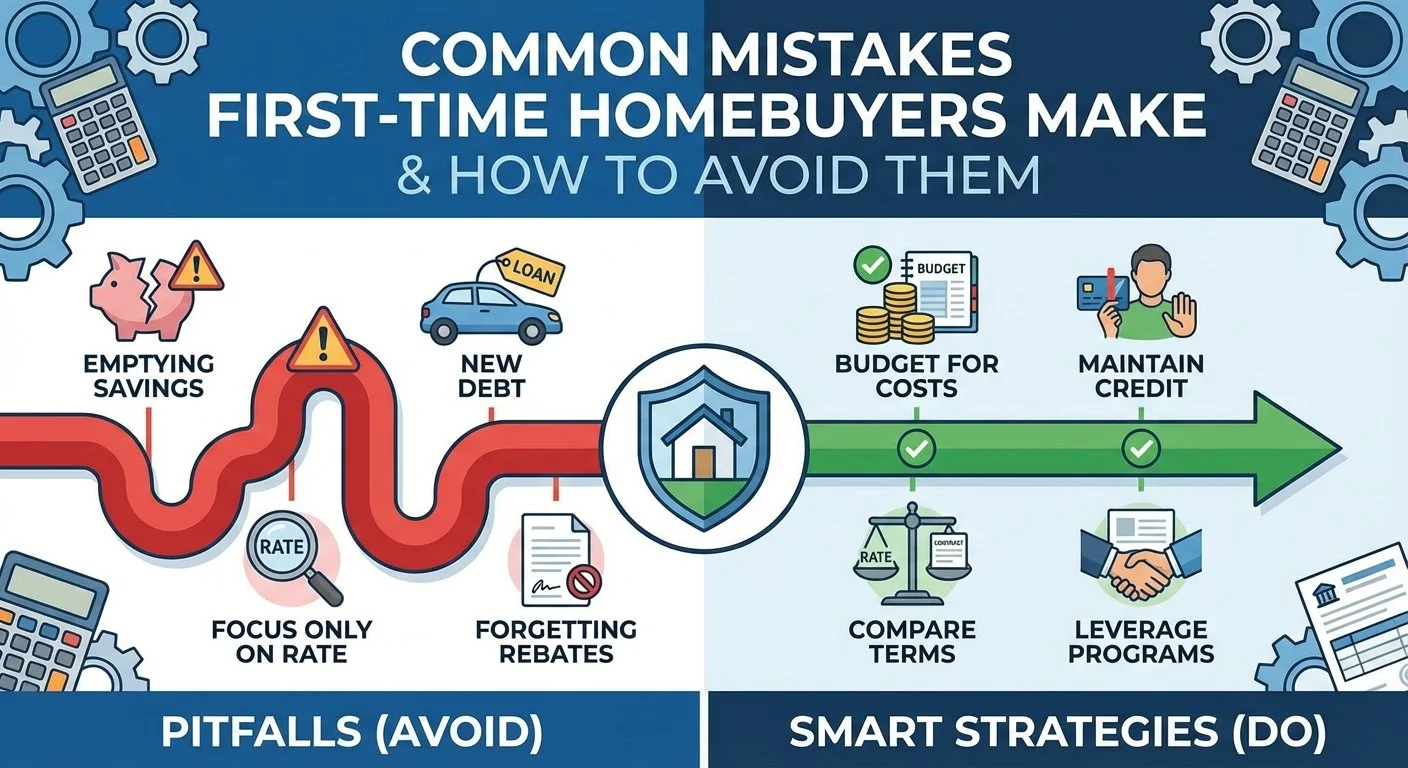

Common Mistakes First-Time Homebuyers Make (And How to Avoid Them)

Emptying Your Savings for the Down Payment: It is crucial to remember that your down payment is not your only upfront cost. You must budget for "closing costs," which typically amount to 1.5% to 2% of the purchase price. These include legal fees, appraisal fees, title insurance, and property tax adjustments.

Taking on New Debt Before Closing: Once you are pre-approved, do not finance a new car, open new credit cards, or co-sign a loan for someone else. Any changes to your credit profile or debt-to-income ratio can cause a lender to revoke your mortgage approval just before closing.

Focusing Only on the Interest Rate: While a low rate is important, the terms of the mortgage are equally vital. A mortgage with a slightly lower rate but harsh, restrictive penalties for breaking the term early can cost you thousands if you need to sell or refinance your mortgage before the term is up. I ensure you get a great rate and flexible terms.

Forgetting About First-Time Buyer Rebates: Many buyers miss out on the First-Time Home Buyers' Tax Credit or fail to structure their RRSP/FHSA withdrawals correctly. I work closely with you to ensure you leverage every available program to keep more money in your pocket.

Schedule Your Mortgage Consultation

Frequently Asked Questions (FAQs) for Vancouver First-Time Buyers

Navigating BC's housing scene? I've got straightforward answers on mortgages, down payments, and government programs—no jargon, just clear insights from 15+ years helping locals like you.

How much of a down payment do I need to buy a home in Vancouver?

In Canada, the minimum down payment depends on the purchase price of the home. For homes under $500,000, the minimum is 5%. For homes between $500,000 and $999,999, you need 5% on the first $500,000 and 10% on the remaining balance. For homes priced at $1,000,000 or more (which is common in Vancouver), a minimum down payment of 20% is strictly required.

What is mortgage default insurance (CMHC insurance)?

If your down payment is less than 20% of the purchase price, you are required by law to purchase mortgage default insurance (often referred to as CMHC insurance, though Sagen and Canada Guaranty also provide it). This insurance protects the lender in case you default on your payments. The premium is calculated as a percentage of your loan and is typically added to your total mortgage balance, so you don't have to pay it upfront in cash.

Can I use gifted money for my down payment?

Yes! Many first-time buyers in Vancouver receive financial help from family members. Lenders allow down payments to be gifted from an immediate family member. However, the lender will require a signed "gift letter" confirming that the money is genuinely a gift and not a loan that requires repayment. I can provide you with the exact templates lenders require.

What is the Mortgage Stress Test?

The mortgage stress test is a federal regulation designed to ensure you can still afford your mortgage payments if interest rates rise. Lenders must qualify you at a rate that is higher than your actual contract rate (typically your contract rate plus 2%, or the benchmark rate of 5.25%, whichever is higher). As your broker, I run these calculations for you upfront so you know exactly what your true buying power is.

Do you only help buyers in Vancouver?

While I am based in North Vancouver and have deep expertise in the Vancouver proper market, I am licensed to assist clients throughout all of British Columbia. Whether you are buying in the Lower Mainland, the Fraser Valley, Vancouver Island, or the BC Interior, I can secure the right financing for you.

Let's Make Your Dream of Homeownership a Reality

Buying your first home is a major financial commitment, but you don't have to navigate it alone. With over 50 lenders at my fingertips and an intimate knowledge of the First-Time Homebuyer Programs available in BC, I will tirelessly match you with the right lender and the best mortgage package suited to your specific needs.

Ready to chat about your Vancouver real estate goals? Drop your details for a no-obligation call. I'll tailor options with my deep local know-how to empower your next move.

Contact Chad Watts Today

Phone:1-778-773-6631

Email:chad@wattsmortgages.ca

Website:www.wattsmortgages.ca

As your dedicated mortgage broker at TMG, my personalized approach ensures that I understand your financial goals. Let's work together to unlock better mortgage terms, maximize your borrowing power, and secure the keys to your first home. Reach out today to start this exciting journey!