Cash-Out Refinancing in 2026: Unlocking Home Equity for Renovations, Investments, or Debt Consolidation

Why Vancouver Homeowners Are Leveraging Equity in 2026

In the dynamic real estate landscape of 2026, Vancouver homeowners are sitting on a powerful asset: their home equity. With property values in the Lower Mainland remaining robust, cash-out refinancing has become a strategic financial tool for many. Whether you are looking to update your home, consolidate high-interest debt, or expand your real estate portfolio, unlocking this equity can provide the liquidity you need without the hassle of selling your property.

As a seasoned Vancouver mortgage broker, I, Chad Watts, have helped countless clients navigate the complexities of refinancing. By breaking your existing mortgage and taking out a new one for a higher amount than you owe, you receive the difference in tax-free cash. This strategy allows you to leverage your home's value to further your financial goals, often at a much lower interest rate than other borrowing options like personal loans or credit cards.

Smart Ways to Utilize Your Cash-Out Refinance

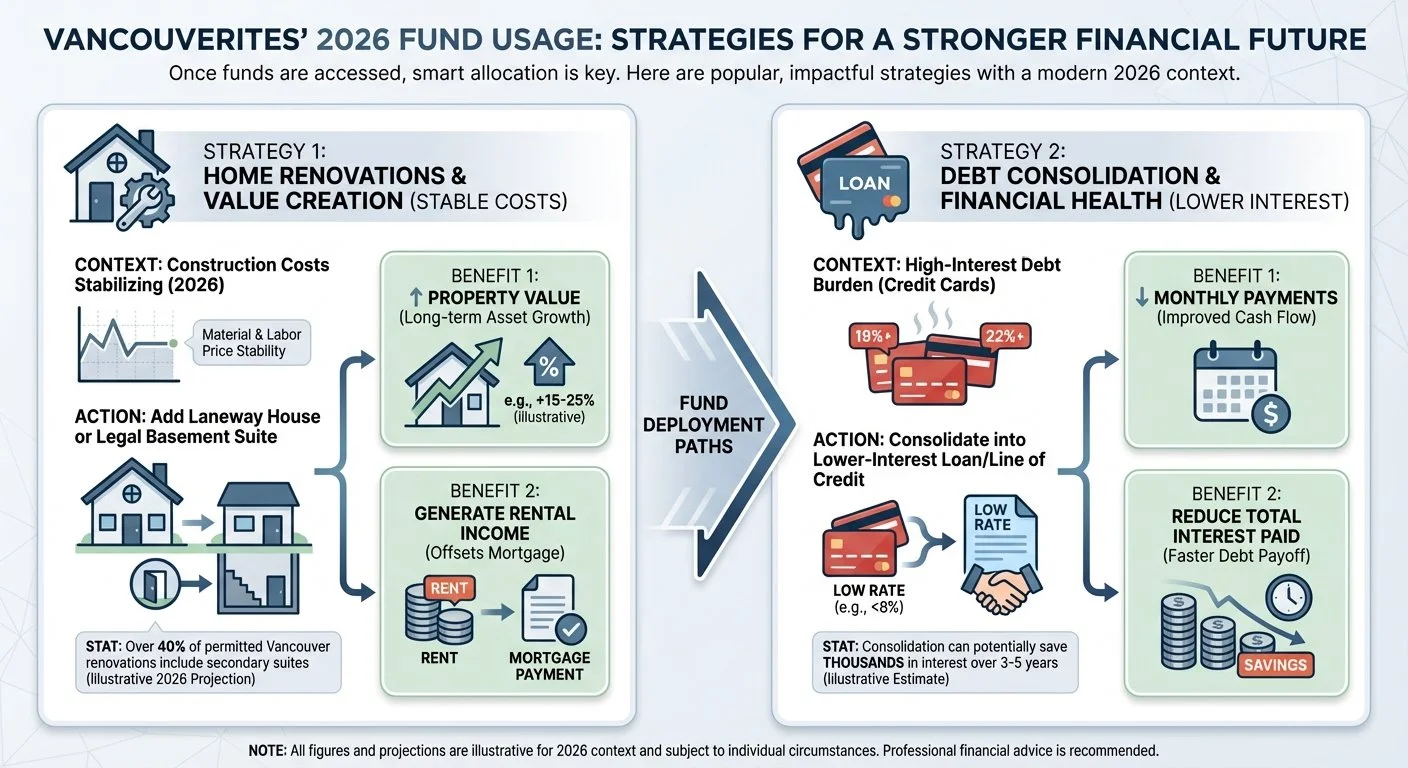

Once you access your funds, how you use them can significantly impact your financial future. Here are the most popular strategies for Vancouverites in 2026:

Home Renovations: With construction costs stabilizing, many homeowners are choosing to renovate rather than move. Adding a laneway house or a legal basement suite not only increases your property value but can also generate rental income to offset mortgage payments.

Debt Consolidation: If you are carrying high-interest debt on credit cards or lines of credit, rolling that balance into your mortgage can save you thousands in interest and drastically reduce your monthly cash flow obligations.

Investment Properties: Using equity as a down payment for a rental property is a classic wealth-building strategy. I specialize in helping clients structure these deals to maximize borrowing power and rental offsets.

At Watts Mortgages, I work with over 50 lenders to ensure that your refinance terms align perfectly with these goals.

Debt TypeInterest Rate (Est.)Monthly Payment on $50,000Credit Cards19.99%$1,500+ (Min. Payment)Personal Line of Credit9.00% - 12.00%$450 - $600 (Interest Only)Mortgage Refinance4.50% - 5.50%$280 - $310 (Amortized)

Navigating the Refinance Process in BC

Refinancing in British Columbia involves specific rules and qualifications. Generally, you can refinance up to 80% of your home's appraised value. This means you must retain at least 20% equity in the property. During this process, you will need to undergo the federal mortgage stress test again to ensure affordability.

This is where working with an expert makes a difference. Unlike a bank that only offers its own products, I shop the market for you. If traditional lenders say no due to self-employment or credit challenges, I have access to alternative and private lenders who focus on equity rather than strict income ratios. My goal is to make the process seamless, handling the paperwork and negotiations so you can focus on your plans.

Whether you are in North Vancouver, Surrey, or right downtown, I provide personalized advice to ensure the costs of breaking your current term—if applicable—are outweighed by the long-term savings and benefits of the new mortgage.

Q1: How much equity can I take out of my home?

In Canada, you can typically refinance up to 80% of your home's current appraised value, minus your existing mortgage balance.

Q2: Are there penalties for refinancing early?

Yes, if you break your mortgage term early, you may face a prepayment penalty. I help you calculate if the savings from refinancing outweigh these costs.

Q3: Can I refinance if I have bad credit?

Absolutely. While major banks may be strict, I have access to B-lenders and private lenders who focus more on your property equity than your credit score.

Q4: What can I use the money for?

The funds are yours to use as you wish—common uses include home renovations, debt consolidation, investment purchases, or funding education.

Q5: How long does the refinancing process take?

Typically, a refinance takes 2 to 4 weeks from application to funding, depending on the lender and appraisal speed.