B-Lender Mortgages in Vancouver: Flexible Solutions for Lower Credit Scores

Securing a mortgage in Vancouver can feel overwhelming, especially if traditional banks have turned down your application due to a lower credit score, non-traditional income, or past financial difficulties. If you have been told "no" by a major bank, it is important to know that you still have excellent options. As an experienced mortgage broker in Vancouver, BC, Chad Watts specializes in connecting individuals with trusted B-lenders who offer flexible, common-sense alternative mortgage solutions.

Do not let a less-than-perfect credit history stop you from achieving your real estate goals. Whether you are looking to purchase a new home, refinance an existing property to consolidate debt, or access your home equity, B-lending provides a strategic pathway forward. With over 15 years of experience navigating the competitive British Columbia real estate market, Chad Watts is here to help you secure the financing you need while building a roadmap to restore your financial health.

What is B-Lending? Understanding Alternative Mortgages

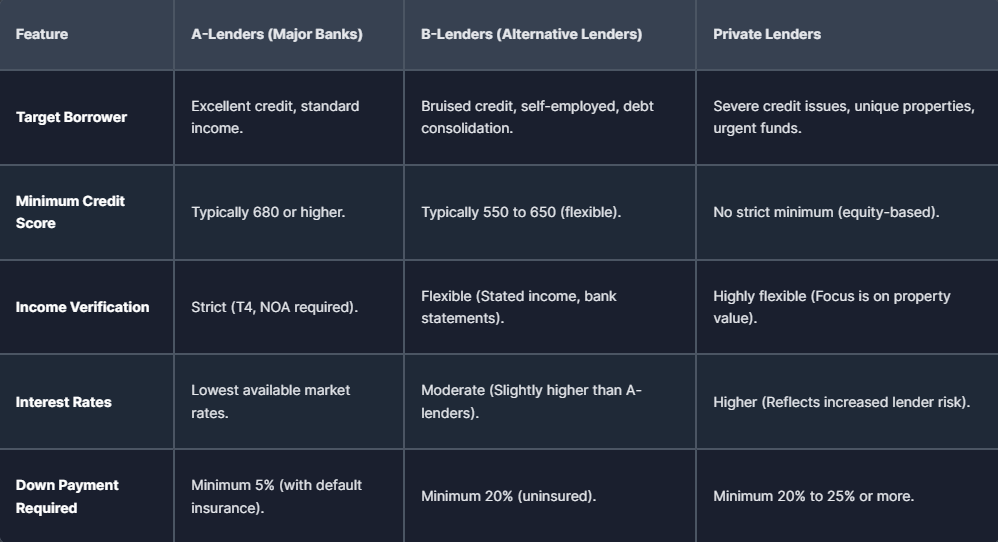

In the Canadian mortgage industry, lenders are generally categorized into three tiers: A-lenders, B-lenders, and Private lenders. A-lenders include the major traditional banks and credit unions. They offer the lowest interest rates but maintain exceptionally strict qualifying criteria, including high credit score requirements and rigid income verification rules.

B-lenders, also known as alternative lenders, include trust companies, specialized mortgage finance companies, and certain credit unions. These institutions are fully regulated but operate with more flexible underwriting guidelines than traditional banks. Instead of relying solely on an automated credit score, B-lenders take a comprehensive look at your overall financial picture. They consider the equity in your property, the stability of your income (even if it is self-employed or non-traditional), and your future financial potential.

A B-lender mortgage is typically used as a short-term stepping stone. The goal is to secure a mortgage for a one to three-year term, use that time to improve your credit score or stabilize your income, and eventually transition back to an A-lender at the end of your term.

Who Can Benefit from a B-Lender Mortgage in BC?

Alternative lending is designed for a wide variety of borrowers who fall outside the strict parameters of traditional bank guidelines. You may be an ideal candidate for a B-lender mortgage if you fit into any of the following categories:

Individuals with Low Credit Scores: If your credit score has dropped due to missed payments, high credit card utilization, or unexpected life events, B-lenders are willing to look past the number and focus on your ability to repay the loan.

Self-Employed Professionals: Traditional banks often require two years of Notice of Assessment (NOA) documents, which can be challenging for business owners who legally minimize their taxable income. B-lenders offer stated-income programs that recognize your true earning potential.

Borrowers with High Debt Ratios: If you carry significant consumer debt, your debt-to-income ratio may exceed standard limits. B-lenders offer extended ratios, allowing you to qualify for a mortgage or refinance to consolidate your high-interest debts into one lower monthly payment.

Life Event Recovery: If you have experienced a divorce, a medical emergency, or a sudden job loss that temporarily impacted your finances, B-lenders offer the second chance you need to get back on track.

Past Bankruptcy or Consumer Proposal: Even if you have a discharged bankruptcy or a completed consumer proposal on your record, B-lenders provide pathways to homeownership much sooner than traditional banks.

Why Choose Chad Watts for Your Alternative Mortgage Needs?

When dealing with credit challenges, having a knowledgeable and unbiased advocate on your side is critical. Chad Watts brings a unique, highly personalized approach to mortgage brokering in Vancouver and North Vancouver.

Over 15 Years of Local Experience: As a native Vancouverite, Chad understands the nuances of the local housing market. He knows what local lenders look for and how to present your application in the best possible light to ensure approval.

Access to 50+ Lenders: Unlike a bank employee who can only offer you one set of products, Chad partners with over 50 banks, trust companies, credit unions, and alternative lenders. This extensive network means he can shop the market on your behalf to find the most competitive rates and terms available for your specific situation.

A Focus on Long-Term Financial Health: Chad does not just secure your alternative mortgage and walk away. He works with you to develop a clear, actionable strategy to improve your credit over the term of your B-lender mortgage, ensuring you are in a prime position to qualify for prime rates in the future.

Transparent and Honest Communication: Mortgages can be complex, especially in the alternative lending space. Chad prides himself on providing straightforward, jargon-free advice. You will always understand your interest rates, any associated fees, and the exact steps required to complete your transaction.

The Strategic Benefits of B-Lending

Choosing an alternative lender offers several distinct advantages for borrowers facing financial hurdles. Understanding these benefits can help you make an informed decision about your real estate financing.

1. Flexible Approval Criteria

The primary benefit of a B-lender is flexibility. These lenders use common-sense underwriting. If you have a solid down payment or significant equity in your home, they are often willing to overlook a bruised credit score or non-traditional income documentation.

2. An Opportunity to Rebuild Credit

A B-lender mortgage is an active credit-building tool. By making your alternative mortgage payments on time, you demonstrate financial responsibility to the major credit bureaus (Equifax and TransUnion). Over a standard two-year term, this consistent payment history can significantly boost your credit score.

3. Debt Consolidation Opportunities

If you are a current homeowner struggling with high-interest credit card debt or personal loans, a B-lender can help you access your home equity. By refinancing and consolidating your debts into your mortgage, you can drastically reduce your monthly outgoing payments, ease your financial stress, and improve your credit utilization ratio.

4. Faster Approvals for Complex Situations

Because B-lenders do not rely entirely on automated, rigid approval algorithms, they can often manually review and approve complex files much faster than a traditional bank trying to fit a unique situation into a standard box.

Comparing Mortgage Options: Traditional vs. Alternative Lending

To help you understand where B-lending fits into the mortgage landscape, review this comparison between A-Lenders, B-Lenders, and Private Lenders.

Our Streamlined B-Lending Process

Navigating the alternative mortgage market does not have to be stressful. Chad Watts has developed a simple, three-step process to help you secure the funds you need efficiently and transparently.

Step 1: Get to Know You (Comprehensive Consultation)

Step 2: Target the Right Lender

Based on the insights gathered during your consultation, Chad will analyze his network of over 50 lenders to find the perfect match. He will identify the B-lenders most likely to approve your specific file, negotiate on your behalf to secure the best possible interest rate, and present you with clear, easy-to-understand options.

Step 3: Secure Your Funds and Plan for the Future

The Transition Strategy: Moving from B-Lender to A-Lender

One of the most important aspects of securing a B-lender mortgage is having a clear exit strategy. A B-lender is a temporary solution, not a permanent home for your mortgage. Chad Watts works closely with his Vancouver clients to ensure they are on the right path to financial recovery.

During your one or two-year term with an alternative lender, Chad will advise you on specific actions to take to improve your lending profile. This may include:

Never Missing a Payment: Ensuring your mortgage, auto loans, and credit card payments are made on time, every single month.

Lowering Credit Utilization: Keeping your credit card balances below 30% of your total available limit to rapidly boost your Equifax and TransUnion scores.

Filing Taxes on Time: For self-employed individuals, ensuring your taxes are filed and up-to-date to show a stable income history.

Avoiding New Debt: Refraining from taking out new vehicle loans or large lines of credit while you are actively trying to rehabilitate your mortgage profile.

As your renewal date approaches, Chad will proactively review your improved financial file and apply to traditional A-lenders on your behalf, helping you secure lower interest rates for your next mortgage term.

Understanding B-Lender Fees and RatesStep 2: Target the Right Lender

Based on the insights gathered during your consultation, Chad will analyze his network of over 50 lenders to find the perfect match. He will identify the B-lenders most likely to approve your specific file, negotiate on your behalf to secure the best possible interest rate, and present you with clear, easy-to-understand options.

Step 3: Secure Your Funds and Plan for the Future

The Transition Strategy: Moving from B-Lender to A-Lender

One of the most important aspects of securing a B-lender mortgage is having a clear exit strategy. A B-lender is a temporary solution, not a permanent home for your mortgage. Chad Watts works closely with his Vancouver clients to ensure they are on the right path to financial recovery.

During your one or two-year term with an alternative lender, Chad will advise you on specific actions to take to improve your lending profile. This may include:

Never Missing a Payment: Ensuring your mortgage, auto loans, and credit card payments are made on time, every single month.

Lowering Credit Utilization: Keeping your credit card balances below 30% of your total available limit to rapidly boost your Equifax and TransUnion scores.

Filing Taxes on Time: For self-employed individuals, ensuring your taxes are filed and up-to-date to show a stable income history.

Avoiding New Debt: Refraining from taking out new vehicle loans or large lines of credit while you are actively trying to rehabilitate your mortgage profile.

As your renewal date approaches, Chad will proactively review your improved financial file and apply to traditional A-lenders on your behalf, helping you secure lower interest rates for your next mortgage term.

Understanding B-Lender Fees and Rates

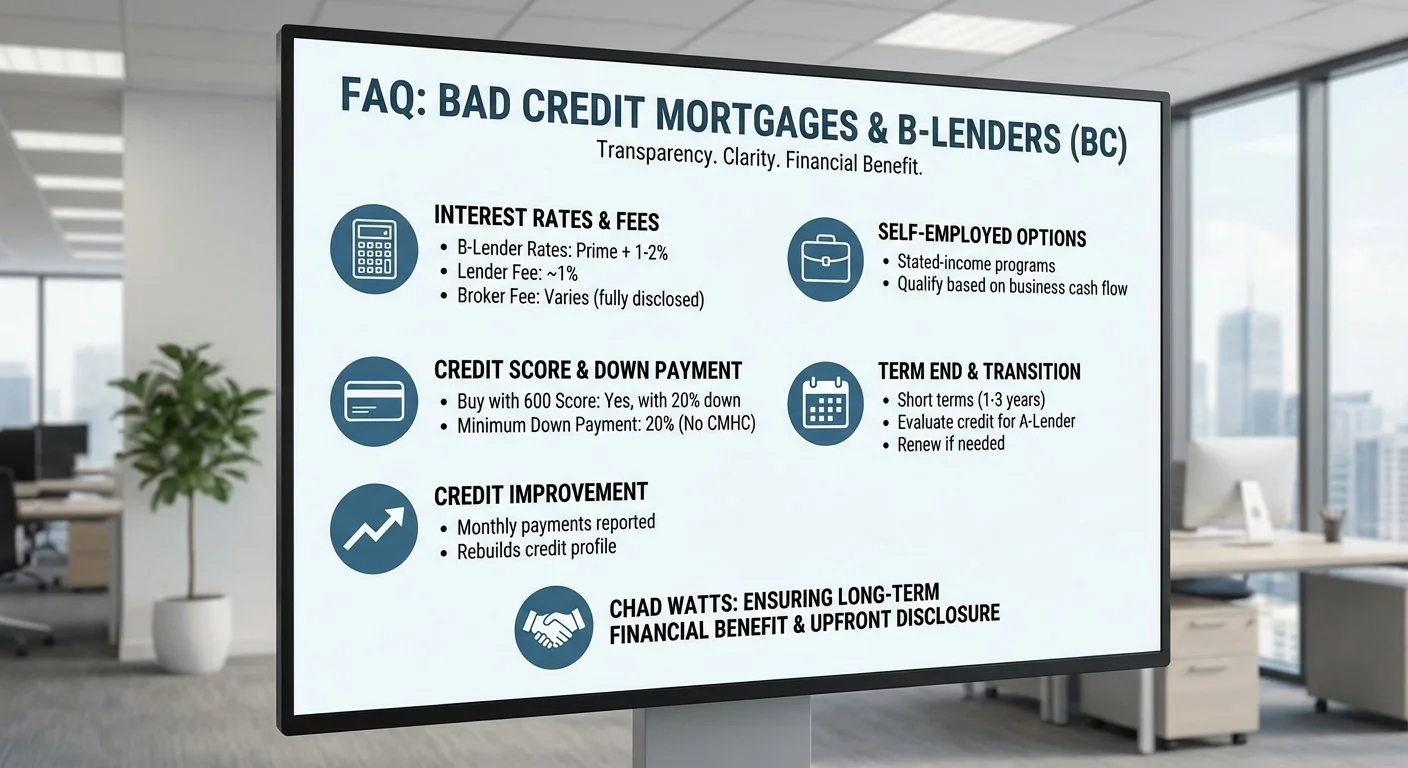

Interest rates for B-lenders are generally 1% to 2% higher than the prime rates offered by major banks. Additionally, alternative lenders typically charge a lender fee, which is usually around 1% of the total loan amount. In some cases, a broker fee may also apply, depending on the complexity of the file. All fees and rates will be fully disclosed to you upfront before you sign any commitments. Chad Watts ensures that the financial benefit of the mortgage (such as saving money through debt consolidation or successfully purchasing a home) far outweighs the short-term costs associated with alternative lending.

Frequently Asked Questions About Bad Credit Mortgages in BC

Can I buy a house in Vancouver with a 600 credit score?

Yes, it is absolutely possible. While traditional banks typically look for a score of 680 or higher, B-lenders routinely approve mortgages for individuals with credit scores between 550 and 650. The key is having a larger down payment (usually 20%) and demonstrating the ability to make your monthly payments.

How much down payment do I need for a B-lender mortgage?

Because B-lender mortgages are not insured by the Canada Mortgage and Housing Corporation (CMHC), you will need a minimum down payment of 20% of the purchase price. If you are refinancing an existing property, you must retain at least 20% equity in the home.

Will a B-lender mortgage help improve my credit score?

Yes. B-lenders report your monthly mortgage payments to the major Canadian credit bureaus. By making your payments on time and in full every month, you will actively rebuild your credit profile, making it easier to qualify for prime lending rates in the future.

Can self-employed individuals use alternative lending?

Alternative lending is an excellent option for self-employed individuals in BC. B-lenders offer stated-income programs that allow business owners to qualify based on their business bank statements and cash flow, rather than relying solely on the net income declared on their personal tax returns.

What happens when my B-lender mortgage term ends?

Most B-lender mortgages are set up on short terms, usually one to three years. As your term approaches its end, Chad Watts will evaluate your current financial situation and credit score. If your credit has improved, he will help you transition your mortgage to a traditional A-lender to secure a lower interest rate. If you need more time, you can often renew with your current B-lender.

Are B-lenders safe and regulated?

Yes. B-lenders are heavily regulated financial institutions in Canada. They include well-known trust companies and credit unions that must adhere to strict provincial and federal financial guidelines. Working with a licensed mortgage broker like Chad Watts ensures you are placed with a reputable, secure lending institution.

Contact Chad Watts: Your Vancouver Alternative Mortgage Expert

If you have been turned away by your bank or are worried that your credit score will prevent you from achieving your homeownership goals, do not give up. Mortgages have changed, and there are innovative solutions available for nearly every financial situation.

Take control of your financial future today by partnering with an expert who understands the Vancouver market and has the lender connections to get your file approved. Chad Watts is dedicated to providing personalized service, unbiased advice, and the strategic guidance you need to succeed.

Ready to explore your B-lending options?

Call Today:1-778-773-6631

Email:chad@wattsmortgages.ca

Location: Serving Vancouver, North Vancouver, and the entire BC Lower Mainland.

Contact Chad Watts today to schedule your free, confidential consultation. Let's work together to find the right financing partner and make your real estate dreams a reality.