Expert B-Lending & Debt Consolidation Mortgages in Vancouver, BC

Living in Vancouver offers an incredible lifestyle, but it also comes with a high cost of living. When unexpected expenses arise, or when the daily cost of managing a household increases, many homeowners find themselves relying on credit cards, lines of credit, or personal loans. Over time, these high-interest debts can accumulate, making it incredibly difficult to manage monthly cash flow and get ahead financially.

If you are a homeowner in Vancouver or the surrounding areas of British Columbia, you have a powerful financial tool at your disposal: your home equity. However, if your credit score has taken a hit due to high debt utilization, or if you have non-traditional income, major banks might turn you down for a standard refinance. This is where B-lending for debt consolidation becomes a life-changing financial strategy.

As a seasoned mortgage broker with over 15 years of experience in the Greater Vancouver market, Chad Watts specializes in connecting clients with alternative mortgage solutions. By leveraging a network of over 50 lenders, Chad helps homeowners consolidate high-interest debt, lower their monthly payments, and create a clear path toward financial recovery.

What is B-Lending?

The Canadian mortgage market is generally divided into three main categories: A-lenders, B-lenders, and private lenders. Understanding the difference is crucial when exploring debt consolidation options.

A-Lenders: These are the major banks and prime credit unions. They offer the lowest interest rates but have the strictest qualification guidelines. Borrowers must pass a rigorous federal stress test, prove traditional verifiable income, and maintain a high credit score. If your debt levels are currently too high, your Total Debt Service (TDS) ratio will likely disqualify you from A-lender financing.

B-Lenders (Alternative Lenders): Alternative lenders include trust companies, specialized credit unions, and alternative mortgage corporations. They are governed by different regulations than major banks, allowing them to offer more flexible qualification criteria. B-lenders focus heavily on the equity you have in your property and are far more forgiving of bruised credit, high debt ratios, and self-employed income.

Private Lenders: These are individuals or investment groups that provide short-term, equity-based financing. They are typically used when both A-lenders and B-lenders decline an application, often serving as a temporary bridge for complex financial situations.

For most Vancouver homeowners looking to consolidate debt, B-lending provides the perfect middle ground. It offers slightly higher rates than a traditional bank, but significantly lower rates than credit cards or unsecured personal loans, all while providing the flexibility needed to get approved.

Why Vancouver Homeowners Choose B-Lending to Consolidate Debt

Debt consolidation involves taking out a new mortgage or a second mortgage to pay off multiple unsecured debts. By rolling your high-interest obligations into one single mortgage payment, you can dramatically improve your financial situation. Here is why alternative lending is a powerful strategy for debt consolidation:

1. Massive Monthly Cash Flow Improvement

Credit cards often carry interest rates of 19.99% to 29.99%. Personal loans and auto loans can also carry steep rates. By paying off these debts with a B-lender mortgage, you are replacing multiple high-interest payments with a single, much lower interest rate. This can easily free up hundreds, or even thousands, of dollars in your monthly budget.

2. Rapid Credit Score Repair

One of the biggest factors determining your credit score is your credit utilization ratio. This is the amount of credit you are using compared to your total available limits. If your credit cards are maxed out, your credit score will plummet. When a B-lender provides the funds to pay those balances down to zero, your credit utilization instantly improves. Many clients see a significant boost in their credit scores within just a few months of consolidation.

3. Flexible Income Verification

Vancouver has a thriving community of entrepreneurs, freelancers, and gig economy workers. Traditional banks often struggle to qualify self-employed individuals because they base approvals on the net income claimed on tax returns. B-lenders offer specialized "stated income" or "bank statement" programs. They look at the actual cash flow of your business to determine affordability, making it much easier for self-employed homeowners to consolidate debt.

4. Avoiding Consumer Proposals or Bankruptcy

When debt becomes unmanageable, some homeowners mistakenly believe their only options are a consumer proposal or bankruptcy. Both of these options will devastate your credit for up to seven years and can severely impact your financial future. If you have equity in your home, a B-lender mortgage can help you pay your creditors in full, protecting your financial reputation and keeping you in your home.

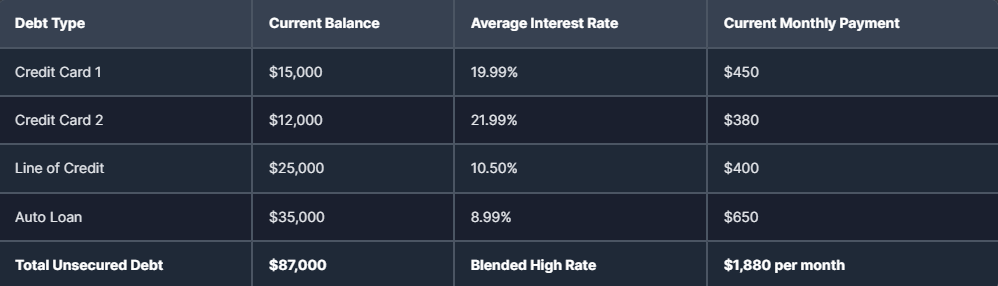

Comparing the Costs: Traditional Debt vs. Alternative Consolidation

The B-Lending Solution: By refinancing the existing mortgage and adding the $87,000 of unsecured debt into a new alternative mortgage, the homeowner eliminates the $1,880 in separate monthly payments. Even if the new B-lender mortgage rate is slightly higher than a prime bank rate, the amortization of the loan over 25 or 30 years means the portion of the mortgage payment covering that $87,000 might only be $500 to $600 per month. This creates an immediate monthly savings of over $1,200, drastically reducing financial stress.

Common Types of Debt You Can Consolidate

Alternative lenders are highly flexible when it comes to the types of debt you can pay off using your home equity. Chad Watts has successfully helped clients across British Columbia consolidate a wide variety of financial obligations, including:

High-Interest Credit Cards: The most common form of toxic debt, often carrying rates near 20%.

Personal Loans and Lines of Credit: Unsecured loans that have become difficult to manage due to rising variable interest rates.

Vehicle Financing: Paying off an expensive car loan to free up immediate monthly cash flow.

CRA Tax Arrears: Traditional banks will automatically decline a mortgage application if you owe back taxes to the Canada Revenue Agency. B-lenders are willing to advance funds specifically to pay off CRA debts and remove tax liens.

Property Tax Arrears: Falling behind on property taxes puts your home at risk. B-lenders can roll these arrears into your new mortgage.

Private Mortgages: If you currently have a high-cost private second mortgage, an alternative lender can often consolidate it into a single, more manageable first mortgage.

The Debt Consolidation Process with Chad Watts

Navigating the alternative lending market requires expertise and local knowledge. As a native Vancouverite and a trusted mortgage broker in North Vancouver, BC, Chad Watts simplifies the process from start to finish. Here is what you can expect when you partner with Watts Mortgages:

Step 1: The Initial Discovery Consultation

The process begins with a comprehensive, no-obligation conversation. Chad will listen to your financial goals, review your current debt load, and analyze your credit profile. This is a judgment-free zone. The goal is to understand your unique situation so that the right solution can be tailored for you.

Step 2: Property Valuation and Equity Assessment

Because B-lenders base their approvals largely on the value of your property, determining your home equity is the next critical step. Chad will help arrange a professional appraisal of your Vancouver home. Generally, alternative lenders will allow you to borrow up to 80% of your home's appraised value.

Step 3: Strategic Lender Matching

Step 4: Approval and Payout of Creditors

Once the lender issues a commitment letter, Chad and his team will guide you through the required paperwork. Upon closing, the lawyer or notary will use the new mortgage funds to pay off your existing mortgage and directly pay off your credit cards, loans, and other debts. You start fresh with a single, manageable payment.

Step 5: The Exit Strategy

Who Qualifies for an Alternative Debt Consolidation Mortgage?

If you have been turned down by your primary bank, do not lose hope. The qualification requirements for B-lenders are designed to help people in real-world situations. To qualify for a debt consolidation mortgage through an alternative lender in BC, you generally need:

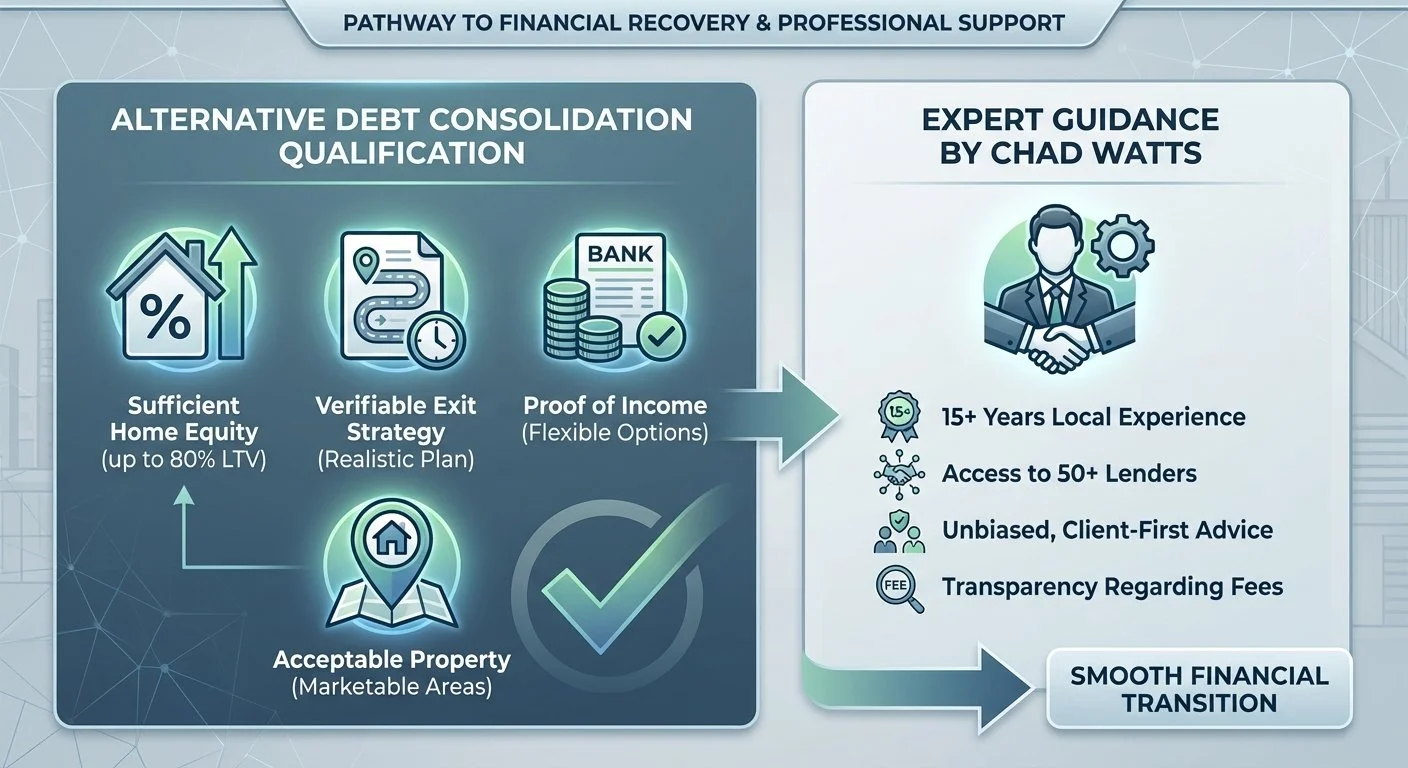

Sufficient Home Equity: You must own a property in BC. Alternative lenders typically lend up to 80% Loan-to-Value (LTV). This means your total new mortgage amount cannot exceed 80% of the current market value of your home.

A Verifiable Exit Strategy: Lenders want to see a realistic plan for how you will eventually transition back to traditional financing or pay off the mortgage.

Proof of Income: While B-lenders are flexible, they still need to ensure you can afford the new consolidated payment. They accept traditional pay stubs, but they also accept bank statements demonstrating business cash flow for self-employed applicants.

An Acceptable Property: The property itself is the primary security for the loan. Homes in highly marketable areas like Vancouver, North Vancouver, Burnaby, Richmond, and the Fraser Valley are highly favored by alternative lenders.

Why Work With Chad Watts for Your B-Lending Needs?

15+ Years of Local Experience: As a seasoned real estate expert and native Vancouverite, Chad has a deep understanding of the BC housing market and the unique challenges local homeowners face.

Access to 50+ Lenders: Chad operates as a true one-stop shop. He has established strong relationships with the top alternative lenders in Canada, ensuring you get access to products that are not available directly to the public.

Unbiased, Client-First Advice: Your bank will never tell you if a competitor down the street has a better offer. Chad works for you, not the lenders. His primary focus is finding the best mortgage solution tailored to your specific financial recovery goals.

Transparency Regarding Fees: Alternative mortgages often come with lender fees and broker fees. Chad believes in 100% transparency. Every cost is clearly explained upfront, with no hidden surprises at closing.

Frequently Asked Questions About B-Lending and Debt Consolidation in BC

Does using a B-lender mean I am using a private lender?

No. While both are alternatives to major banks, they are very different. B-lenders are regulated financial institutions, trust companies, and credit unions. They offer terms and rates that are much closer to bank rates than private lenders. Private lenders are typically individuals or syndicates that charge significantly higher rates and fees. Chad Watts will always attempt to qualify you with a B-lender before ever suggesting a private mortgage.

Will consolidating my debt hurt my credit score?

In the very short term, applying for a new mortgage will result in a hard credit inquiry, which can cause a minor, temporary dip in your score. However, the long-term benefits are overwhelmingly positive. By paying off maxed-out revolving debts (like credit cards), your credit utilization ratio will drop immediately. This is the fastest way to trigger a substantial increase in your credit score.

How much equity do I need in my Vancouver home to consolidate debt?

Most alternative lenders require you to retain at least 20% equity in your home. This means the maximum you can borrow (including your existing mortgage balance and the debts you want to consolidate) is 80% of your home's appraised value. In some specific cases, there may be options to go slightly higher, but 80% is the standard threshold.

What are the fees associated with alternative lenders?

Unlike A-lender mortgages, which typically have no direct fees to the borrower, B-lender mortgages usually involve a lender fee (often around 1% of the loan amount) and a broker fee. You will also need to cover standard closing costs, such as an appraisal and legal fees. The great news is that these fees can almost always be rolled into the new mortgage, meaning you do not have to pay for them out of pocket.

Can I consolidate debt if I am self-employed and show low income on my taxes?

Yes. This is one of the primary benefits of alternative lending. B-lenders understand that business owners often use legal tax write-offs to minimize their declared income. Instead of relying solely on your Notice of Assessment (NOA), alternative lenders can review your business bank statements for the past 6 to 12 months to determine your true gross revenue and ability to service the mortgage.

How long will I have to stay with a B-lender?

Alternative mortgages are typically set up on 1-year or 2-year terms. The goal is never to keep you with a B-lender permanently. Once your debts are consolidated and your credit score has recovered (usually within 12 to 24 months), Chad Watts will proactively reach out to refinance your mortgage back to a prime A-lender at standard bank rates.

Take Control of Your Finances Today

You do not have to lie awake at night worrying about high-interest debt, maxed-out credit cards, or missed payments. The equity you have built in your Vancouver home is a powerful asset that can be used to reset your financial foundation. Mortgages have changed, and there are more flexible solutions available today than ever before.

With expert guidance from Chad Watts, you can navigate the alternative lending market safely, consolidate your debts into one affordable monthly payment, and start rebuilding your credit immediately.

Ready to explore your debt consolidation options? Getting started is simple, entirely confidential, and comes with no obligation.

Contact Chad Watts, Mortgage Broker at TMG

Phone: 1-778-773-6631

Email: chad@wattsmortgages.ca

Website: www.wattsmortgages.ca

Proudly serving Vancouver, North Vancouver, and the entire Greater Vancouver Area. Let's work together to optimize your mortgage, eliminate high-interest debt, and put more money back in your pocket. Reach out today to schedule your free consultation!