Self-Employed Mortgages in Vancouver: B-Lending Solutions for Non-Traditional Income

As a business owner, entrepreneur, or freelancer in Vancouver, BC, you work tirelessly to build your success. However, when it comes time to buy a home, purchase an investment property, or refinance your current mortgage, traditional banks often penalize you for the very tax strategies that help your business thrive. If your tax returns do not reflect your true earning power, securing a traditional mortgage can feel impossible.

At Watts Mortgages, we believe your entrepreneurial spirit should be rewarded, not restricted. Led by Chad Watts, a native Vancouverite and mortgage broker with over 15 years of local experience, we specialize in B-lending solutions for self-employed individuals with non-traditional income reporting. With access to over 50 banks and alternative lenders, we help you bypass the rigid requirements of major banks and secure the financing you deserve.

The Self-Employed Mortgage Challenge: Why Traditional Banks Say No

For standard wage earners, mortgage approval is straightforward. Banks look at a T4 slip and base their lending decisions on gross income. For self-employed individuals, the process is entirely different. Traditional banks, known as A-lenders, typically look at Line 15000 (net income) on your Notice of Assessment to determine your borrowing capacity.

Smart business owners legally write off expenses to minimize their tax burden. While this is excellent for your business cash flow, it drastically reduces your declared net income on paper. As a result, your debt-to-income ratio appears artificially high to a traditional bank, leading to reduced borrowing limits or flat-out rejections.

This is where alternative mortgage solutions, specifically B-lending, become an essential tool for self-employed homebuyers in Vancouver and the Lower Mainland.

What is B-Lending for Non-Traditional Income?

B-lending refers to mortgages provided by alternative financial institutions, such as trust companies, credit unions, and specialized mortgage investment corporations. Unlike traditional A-lenders that are strictly regulated by federal stress tests and rigid income verification rules, B-lenders offer flexible, common-sense underwriting.

Instead of relying solely on your Notice of Assessment, B-lenders utilize stated income or alternative income verification methods. They look at the bigger picture of your financial health, focusing on your business cash flow, bank statements, and overall assets to determine your true ability to service a mortgage.

How B-Lenders Verify Self-Employed Income

Business Bank Statements: Lenders will review 6 to 12 months of your business bank statements to assess consistent cash flow and gross revenue.

Add-Backs: Certain business expenses that reduce your net income but do not affect your actual cash in hand (such as vehicle allowances, home office deductions, or depreciation) can be added back to your income for qualification purposes.

Stated Income Declarations: You declare your reasonable actual income based on your industry and business size, supported by secondary documentation.

Invoices and Contracts: For freelancers and contractors, ongoing service agreements and paid invoices serve as proof of stable revenue.

Who Can Benefit from a Self-Employed Alternative Mortgage?

Our non-traditional income mortgage solutions are designed for a wide variety of professionals across British Columbia who do not fit the standard T4 mold. You may be a perfect candidate for a B-lender mortgage if you are a:

Sole Proprietor or Freelancer: Graphic designers, consultants, and gig economy workers with fluctuating seasonal income.

Incorporated Business Owner: Entrepreneurs who leave money inside their corporation rather than paying themselves a high personal salary.

Tradesperson or Contractor: Construction workers, electricians, and plumbers who write off significant equipment and vehicle expenses.

Commission-Based Earner: Real estate agents, sales professionals, and brokers whose income varies month to month.

Comparing Mortgage Options: A-Lenders vs. B-Lenders

Understanding the difference between traditional and alternative lending is crucial for making an informed decision about your home financing. Below is a comparison to help you understand why B-lending is often the superior choice for business owners.

Schedule Your Mortgage Consultation

The Benefits of Using a B-Lender for Your Vancouver Mortgage

Maximize Your Borrowing Power: By using your gross business revenue rather than your net taxable income, you can qualify for a larger mortgage, allowing you to purchase the home you truly want in Vancouver's competitive real estate market.

Keep Your Tax Strategy Intact: You do not have to artificially inflate your personal income and pay thousands in unnecessary taxes just to appease a traditional bank. Keep your corporate tax strategy in place while still securing property.

Overcome Credit Challenges: Running a business can sometimes lead to temporary credit dips due to high utilization of business credit cards or late client payments. B-lenders are far more forgiving of credit blemishes and focus on the equity in the property and your current cash flow.

Short-Term Stepping Stones: A B-lender mortgage does not have to be forever. We often use alternative lending as a 1 to 3 year short-term solution. Once your business financials align with traditional requirements, we can transition you back to an A-lender at a lower interest rate.

Our Streamlined 3-Step Mortgage Process

Getting a mortgage with non-traditional income reporting does not have to be stressful. At Watts Mortgages, we handle the heavy lifting so you can focus on running your business. Here is how our simple process works:

1. Comprehensive Consultation

2. Target the Right Lender

As an unbiased mortgage broker, I do not work for the banks; I work for you. Based on the insights gathered during our consultation, I will leverage my network of over 50 banks, credit unions, and alternative lenders to find the perfect match for your non-traditional income profile. I will negotiate the best terms, rates, and conditions on your behalf.

3. Secure Your Funds

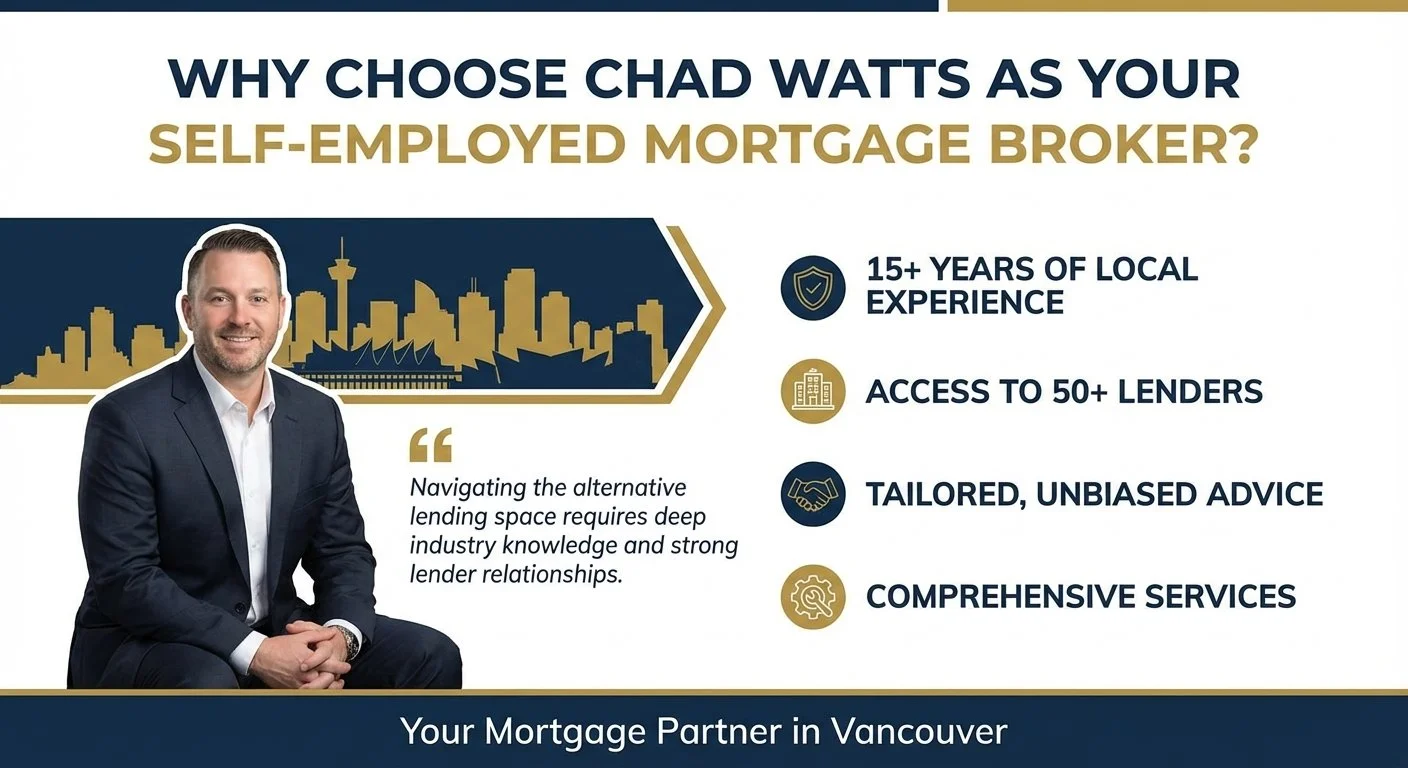

Why Choose Chad Watts as Your Self-Employed Mortgage Broker?

Navigating the alternative lending space requires deep industry knowledge and strong lender relationships. Here is why Vancouver business owners trust Chad Watts with their mortgage needs:

15+ Years of Local Experience: As a native Vancouverite and seasoned real estate expert, I understand the nuances of the BC housing market and the unique challenges local business owners face.

Access to 50+ Lenders: Unlike a bank teller who can only offer you one set of products, I provide a one-stop shop. If a traditional bank says no, I have dozens of alternative and private lending options ready to say yes.

Tailored, Unbiased Advice: My priority is finding the mortgage that fits your life, not pushing a specific bank's agenda. I will clearly explain your options, including fees and interest rates, so there are no surprises.

Comprehensive Services: Whether you are looking for a home purchase, exploring refinancing and renewals, or seeking to consolidate business debt, I have the expertise to structure the deal correctly.

Frequently Asked Questions About Self-Employed Mortgages

Do B-lenders charge higher interest rates?

Yes, because alternative lenders take on more risk by bypassing traditional income verification, their interest rates are typically higher than A-lenders. They may also charge a lender fee (usually 1% of the mortgage amount). However, the cost of these slightly higher rates is often much lower than the extra income tax you would have to pay to declare enough personal income to qualify at a traditional bank.

How much of a down payment do I need for a self-employed B-lender mortgage?

Because B-lenders use alternative income verification, they require a larger equity buffer to mitigate risk. You will typically need a minimum down payment of 20% for a purchase. If you are refinancing an existing property, B-lenders will usually allow you to borrow up to 80% of the home's appraised value.

What documents do I need to provide?

While you get to skip the strict T4 requirements, you will still need to prove your business is active and generating revenue. Common documents include your Articles of Incorporation or Master Business License, 6 to 12 months of business bank statements, a recent Notice of Assessment (to confirm you do not owe income tax arrears), and occasionally a letter from your accountant.

Can I ever move back to a traditional bank?

Absolutely. Many of our self-employed clients use a B-lender for a 1 or 2-year term. During this time, we work together to optimize your tax reporting and improve your credit score. When your term is up for renewal, our goal is to transition your mortgage back to a prime A-lender at the lowest possible market rate.

Ready to Secure Your Self-Employed Mortgage in Vancouver?

Do not let traditional banks dictate your ability to own real estate. If you have non-traditional income reporting, fluctuating revenue, or extensive business write-offs, there is a specialized mortgage solution waiting for you. Mortgages have changed, and it is time to get the latest solutions with the right financing partner.

Let's work together to make your dream of homeownership or property investment a reality. Reach out today to start this exciting journey with a trusted mortgage broker in North Vancouver, BC.

Contact Watts Mortgages Today

Phone: 1-778-773-6631

Email: chad@wattsmortgages.ca

Location: Vancouver, BC

Schedule Your Free, No-Obligation Consultation Now

Disclaimer: Mortgage rates, terms, and approval criteria are subject to change based on lender policies and individual applicant qualifications. Contact Chad Watts for the most current information tailored to your specific financial situation.