The Ultimate Guide to Refinancing Your Mortgage in 2026: Timing, Benefits, and Strategies Amid Stabilizing Rates

Why 2026 Offers a Unique Window for Vancouver Homeowners

After years of rate volatility, 2026 is shaping up to be a year of stabilization for the Canadian housing market. For homeowners in Vancouver, BC, this shift presents a strategic opportunity to revisit existing mortgage terms. Whether you locked in at a peak rate a few years ago or are watching your renewal date approach, the current landscape offers potential for significant savings and improved cash flow.

As a native Vancouverite and experienced mortgage broker, I have seen how local market nuances affect borrowing power. With property values in the Lower Mainland holding strong, many homeowners have accumulated substantial equity. Refinancing in 2026 isn't just about chasing a lower rate; it is about restructuring your debt to align with your long-term financial goals, whether that involves purchasing an investment property or simply reducing your monthly obligations.

Key Benefits: Lowering Payments and Unlocking Equity

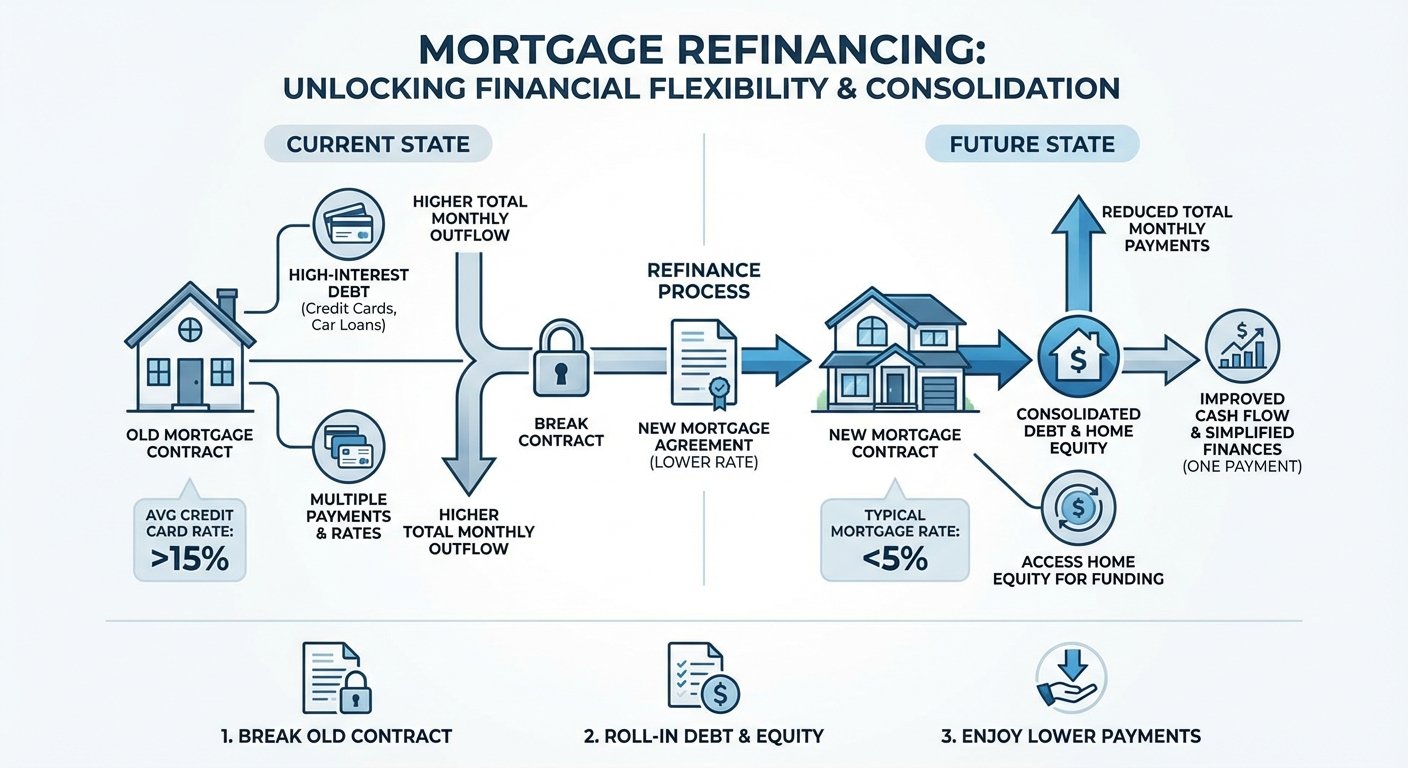

Refinancing allows you to break your current mortgage contract to start a new one, often with more favorable terms. The primary driver for many is debt consolidation. By rolling high-interest consumer debt (like credit cards or car loans) into your mortgage rate—which is typically much lower—you can drastically reduce your total monthly payments. This strategy improves your immediate cash flow and simplifies your finances into one manageable payment.

Additionally, accessing home equity can fund major life projects. Whether you are looking to fund a renovation to increase your property value or need a down payment for a rental property purchase, refinancing allows you to tap into up to 80% of your home's value. Unlike a standard renewal, which just rolls over your balance, a refinance puts your home's appreciation to work for you. With access to over 50 lenders, I can help you find the product that maximizes this leverage without hidden fees.

| Debt Type | Interest Rate (Avg) | Monthly Payment | After Consolidation (Refinance) |

|---|---|---|---|

| Credit Cards ($20k) | 19.99% | $600 | Included in Mortgage |

| Car Loan ($30k) | 8.50% | $550 | Included in Mortgage |

| Mortgage ($500k) | 5.00% | $2,900 | $3,150 (New Total) |

| Total Monthly | - | $4,050 | $3,150 |

Navigating Penalties and Choosing the Right Lender

One of the biggest hesitations homeowners face is the penalty for breaking a mortgage early. In Canada, this is typically calculated as the greater of three months' interest or the Interest Rate Differential (IRD). However, in a stabilizing 2026 market, the long-term interest savings often outweigh the upfront penalty. It is crucial to run the numbers accurately before proceeding.

This is where working with a broker becomes essential. While big banks may only offer their own posted rates, I shop across 50+ banks and financial institutions to find lenders who might offer to cover some of your switching costs or provide lower penalties. If traditional lending isn't an option due to credit challenges, we can also explore private lending options to bridge the gap. My goal is to ensure the math works in your favor, putting more money back in your pocket.

Q1: What is the difference between refinancing and renewing?

Renewing happens when your term ends and you sign on for a new term with the remaining balance. Refinancing involves breaking your current term to change the loan amount, amortization, or rate, often to access equity or lower payments.

Q2: How much equity can I take out of my home in Vancouver?

In Canada, you can typically refinance up to 80% of your home's appraised value, minus the remaining balance of your current mortgage.

Q3: Are there fees for using a mortgage broker for refinancing?

Generally, no. For standard residential mortgages, the lender pays the broker a referral fee. If private lending is required, there may be a broker fee, which is disclosed upfront.

Q4: Can I refinance if I have bad credit?

Yes, it is often possible. While major banks have strict criteria, we have access to alternative and private lenders who focus more on equity than credit score.

Q5: Will refinancing affect my credit score?

Refinancing requires a credit check, which may cause a small, temporary dip in your score. However, consolidating high-interest debt often improves your score in the long run by lowering utilization.

Contact Chad Watts today for a free mortgage review and see how much you can save in 2026!